A New Data Gap: Why Dual-Fuel Technology Is Crucial Now

In both the bulk carrier and tanker sectors, dual-fuel technology is no longer a niche design choice—it is evolving into a structural force that will reshape ship performance, emissions, and fleet competitiveness over the next decade.

The latest order data from VesselsValue reveals a widening gap: while both sectors are experimenting with alternative fuels, their pace of adoption, fuel choices, and business drivers differ significantly, creating two distinct adoption curves.

The Current State of Dual-Fuel Adoption in Tankers: Slow Now, But a Structural Shift is Coming

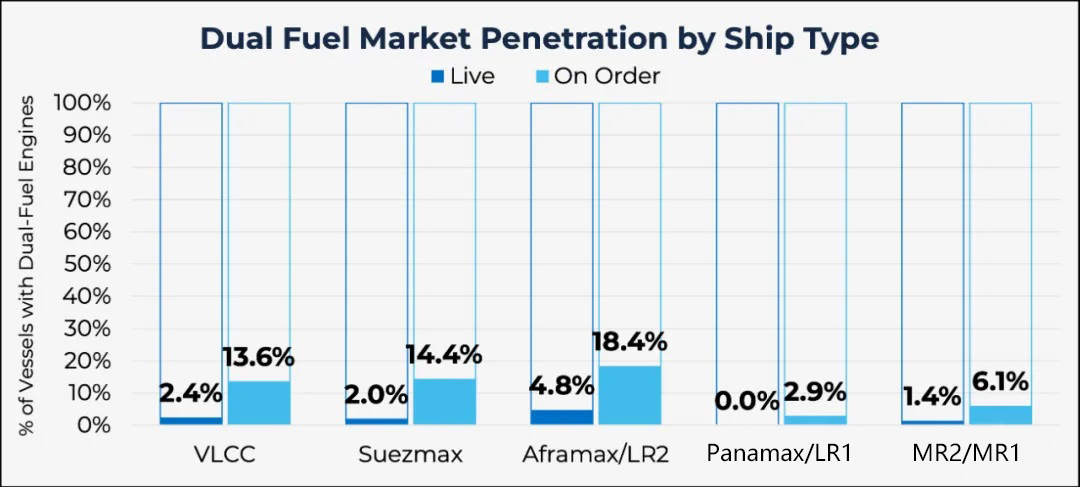

Dual-fuel penetration in the current tanker fleet remains low—ranging from 0% to 4.8% depending on vessel type—but order data tells a different story.

Aframax/LR2 type tankers lead the wayTable 1: Market Penetration of Dual-Fuel Vessels by Ship Type

(Operating Vessels / Orders on Hand)

18.4% of ordered Aframax/LR2 tankers are dual-fuel.

Suezmax: 14.4%

VLCC: 13.6%

There are clear regulatory drivers at play behind this: tightening of the ship energy efficiency index (CII), anticipated carbon pricing mechanisms, and pressure from charterers on emissions performance.

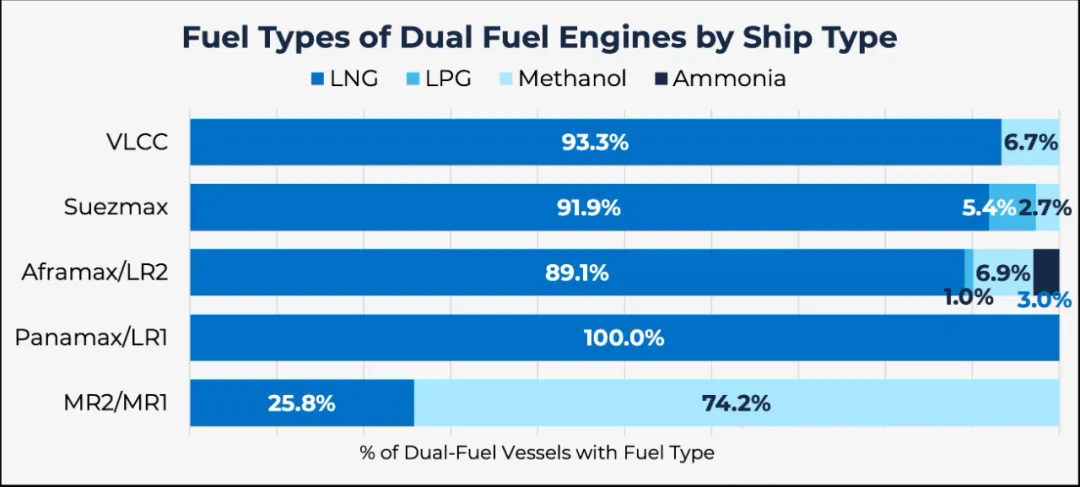

LNG dominates – with only one ship type as an exception.

Table 2: Fuel Type Distribution of Dual-Fuel Engines for Various Ship Types

In overall tanker orders:

93.3% of dual-fuel VLCCs → use LNG

91.9% Suezmax → LNG

89.1% Aframax/LR2 → LNG

However, MR2/MR1 product tankers have broken this pattern:

74.2% of dual-fuel orders → choose methanol instead of LNG.

This reflects commercial synergy—MR-size tankers are closely associated with methanol cargo transportation, making shipowners more familiar with methanol fuel and more likely to obtain refueling at key ports.

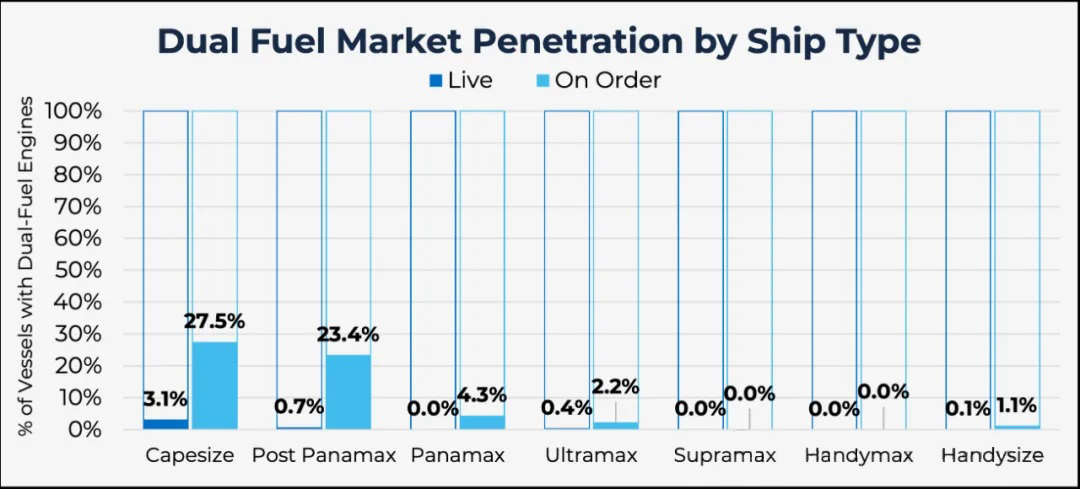

Bulk carriers overtake tankers: Capesize vessels lead the dual-fuel transition

In contrast, the adoption rate of (dual-fuel technology) is significantly higher in the bulk carrier sector, especially in larger vessels.

Capesize vessels lead the entire shipping industry

Table 3: Market Penetration Rate of Dual-Fuel Ships by Type

(Operating Vessels / Orders on Hand)

3.1% of the active fleet has adopted dual-fuel technology.

27.5% of orders are for dual-fuel vessels.

This makes Capesize vessels the fastest-growing segment in the commercial vessel market in terms of dual-fuel transition.

Why the surge?

It's because the underlying drivers are different. Mining giants—BHP, Rio Tinto, Fortescue, Anglo American—are driving orders by demanding long-term charters with cleaner specifications.

Their predictable long-haul routes (Brazil/Australia → China) have also streamlined the logistics of alternative fuels, making LNG, methanol, and even ammonia fuels viable options.

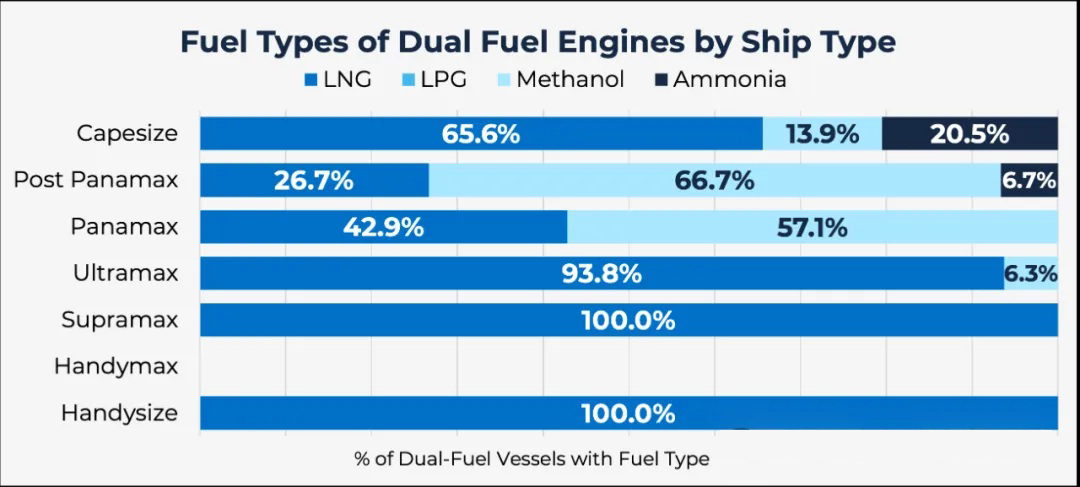

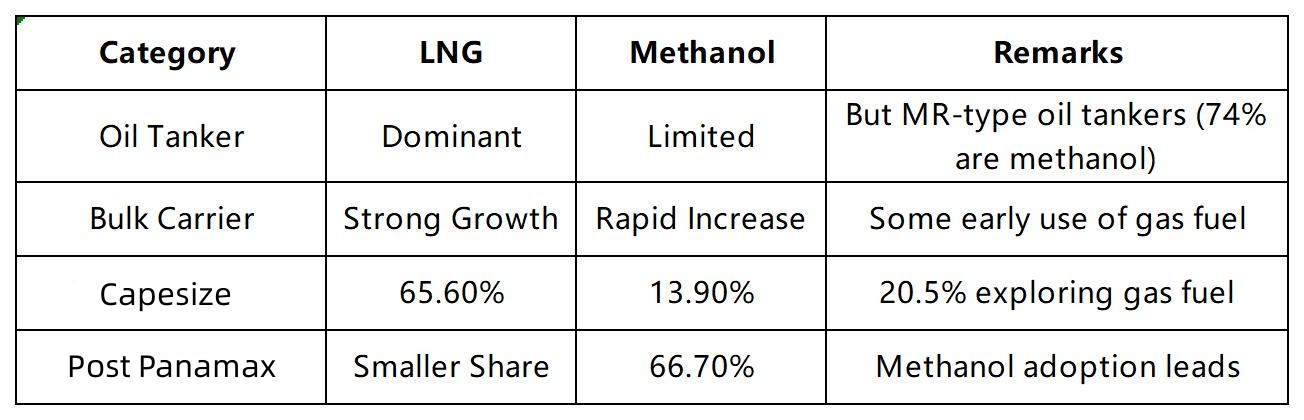

Bulk carriers have significantly different fuel preferences.

Table 4: Fuel Type Distribution for Dual-Fuel Ships of Various Ship Types

Capesize: LNG 65.6% | Methanol 13.9% | Ammonia Fuel Exploration Intent 20.5%

Post-Panamax: Methanol 66.7% (This ship type shows the strongest willingness to adopt methanol)

Panamax: LNG (42.9%) and methanol (57.1%) are developing in parallel

Very Large Handysize/Handysize: LNG is the mainstay (100%), although the actual application rate is still at a low level.

This diversity of fuel choices reflects the bulk carrier sector's more proactive approach to exploring multiple fuel pathways.

Why Tankers are Lagging Behind: The Impact of Trade Patterns and Stakeholder Pressures

Bulk carrier operations are linked to mining contracts, with fixed and predictable routes; while tanker trade patterns are more variable and globalized. This makes fuel infrastructure planning more complex.

Furthermore, the ESG pressures faced by oil giants and commodity traders differ from those faced by global miners, which slows down the adoption of alternative fuel designs in the tanker sector.

A Two-Tier Fleet is Emerging: Winners and Stranded Assets

As dual-fuel vessels rapidly gain popularity in larger vessel types, the global fleet is quietly splitting into two performance tiers:

1. Future-Oriented Vessels

Lower emissions

Preferred by charterers with sustainability requirements

Possessing a more favorable position in tightening energy efficiency indicators (CII) and carbon tax policies

Potentially higher returns and asset value

2. Older, Traditional Vessels

Potentially at a competitive disadvantage in future charter markets

Facing commercial obsolescence risks on regulated routes

Facing higher fuel cost pressures

Increasingly limited opportunities to secure long-term contracts

This differentiation will become increasingly pronounced as the 2026-2030 regulatory cycle expands the application of carbon pricing and operating intensity rules.

Fuel Pathway Battle: Methanol vs. LNG – The Winner is Yet to Be Decided

Different shipping segments are betting on different fuel options:

There is currently no single transition path—fuel choice actually reflects a comprehensive consideration of trade patterns, charterer pressures, fuel availability, and emissions reduction strategies.

What does this mean for shipowners and charterers?

Dual-fuel technology is no longer a technological experiment, but a key factor in commercial differentiation.

For shipowners:Newbuilding decisions must consider long-term carbon risks.

Dual-fuel engines may bring future charter premiums.

Traditional vessels face the risk of accelerated obsolescence.

For charterers:Compliance pressures will increasingly influence fleet selection.

Emissions data transparency will become a mandatory requirement.

Long-term contracts will favor vessels with alternative fuel capabilities.

Looking ahead: A rapidly evolving competitive landscape.

VesselsValue data shows that in the next 3-5 years, as dual-fuel newbuildings begin large-scale deliveries, the bulk carrier and tanker markets will experience significant changes in the following areas:

Environmental performance

Voyage economics

Asset value differentiation

Shifting charterer preferences

Fleet stratification

Against the backdrop of increasingly stringent global emissions regulations, shipowners who plan ahead will occupy a more advantageous commercial position.